Real Estate Marketing & Beyond

No single age group was spared by the recent recession, but for older Americans who were counting on their fixed income lasting throughout their retirement, things have become particularly difficult.

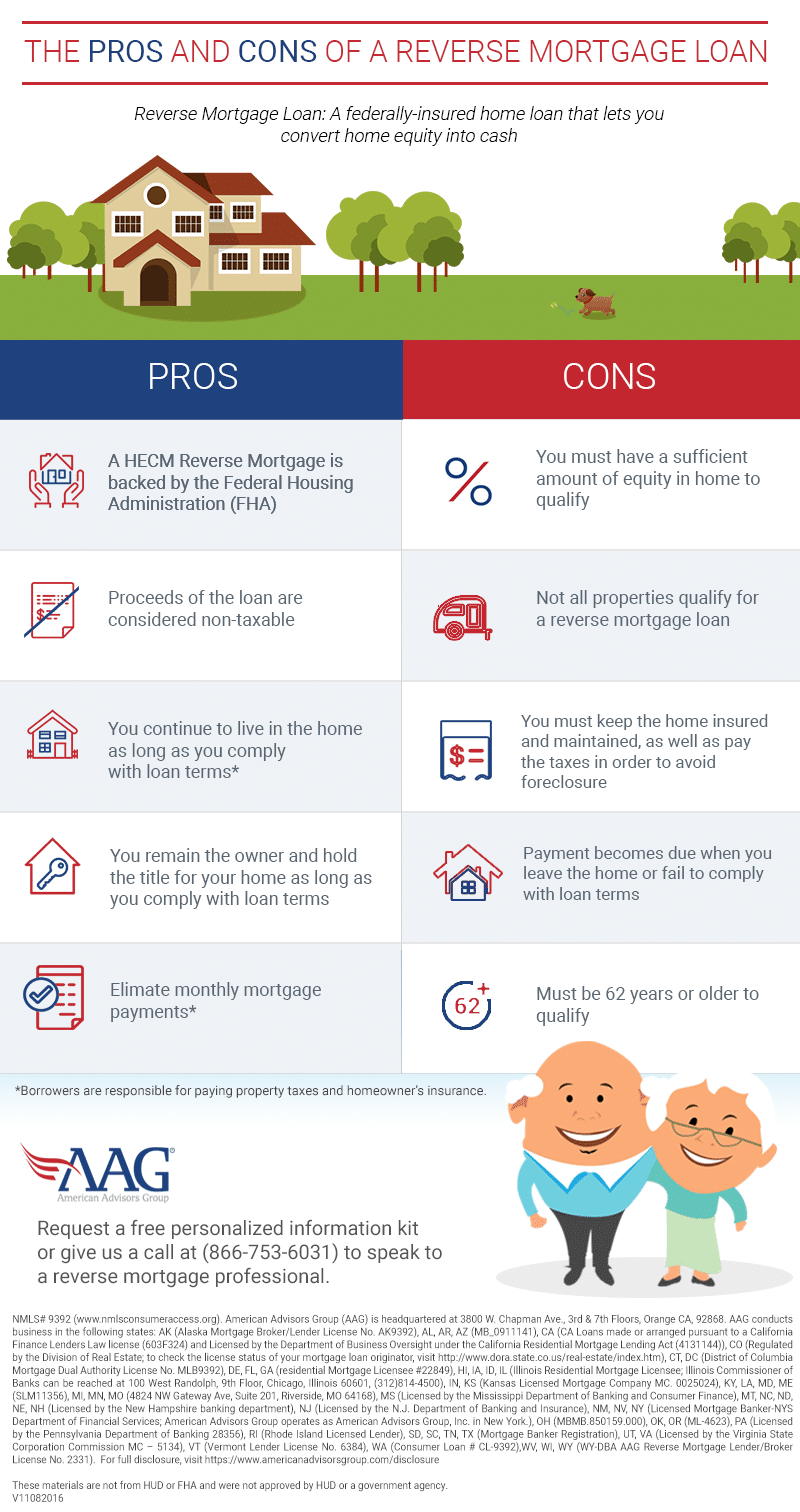

As such, a growing number of senior Americans are considering a reverse mortgage as a way of supplementing their income during their golden years. More than a million borrowers have already taken out this kind of home equity loan, which was created specifically for seniors. But while they might be useful, borrowers should beware that a reverse mortgage loan isn’t right for everyone. As such, it pays to educate yourself about the ins and outs of this type of loan, before coming to a decision if it’s the right solution for you.

What is a reverse mortgage?

A Home Equity Conversion Mortgage, also known as the HECM reverse mortgage, is a loan that functions as a federally-insured cash advance on a borrower’s home equity, and, while there are other maturity events as well, it is repaid when the last borrower leaves the home. They are essentially home loans for homeowners ages 62 and older, and like any loan, there are pros and cons of reverse mortgages.

These are just a few pros and cons of reverse mortgage for seniors ages 62 years and older to consider, and many senior homeowners agree that the positives outweigh the negatives when comparing them.