Real Estate Marketing & Beyond

Valuing residential rental properties can be tricky. Market value is not the same as investment value. When it comes to valuing residential rentals, you're much better off taking the approach that commercial real estate investors use than the approach used by homeowners. Commercial investors base property values on the amount of annual income the property will produce. Homeowners value houses based on what others in the market are paying for similar houses.

To understand the value of investment property you need to understand how to calculate the "cap rate". Not only does this give you a reliable way of understanding your return on investment, it also gives you an apple to apple method of determining the better rate of return between multiple investment options.

© allapen - Fotolia.com

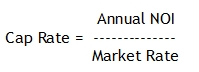

The cap rate is a common ratio used by brokers, sellers, lenders, and other real estate professionals to assign a value to income producing property. The cap rate is derived from the income and expenses generated by the property along with the selling price. The basic formula is:

NOI is Net Operating Income.

Market Rate can be the seller's asking price or your offering price.

Just because a seller is making a monthly profit after paying the mortgage and other expenses doesn't mean you will. Likewise, the annual NOI isn't likely to remain the same under new management. You may be able to reduce expenses or increase rents. Although the formula is easy to calculate, the variables involved can be complex. Never take the seller's stated cap rate at face value. You MUST do your own cap rate calculation.

The trick to determining an income property cap rate is having access to reliable gross income and operating costs.

Gross Income - Operating Expenses = Net Operating Income

Common operating expenses for income property include employee salaries, property taxes, maintenance & supplies, utilities, advertising, insurance, and property management fees. They don't include mortgage, interest, broker commissions, or any costs paid to purchase the property.

However, I suggest making at least two NOI calculations. One that includes the mortgage and interest along with one that does not include the mortgage and interest. The mortgage and interest is excluded in a traditional cap rate calculation because these are variables that will change the result. When a seller or broker quotes a cap rate, they have no way of knowing what a buyer's loan costs are going to be. As the buyer, you want an apple to apple comparison of multiple investment properties and the difference in mortgage and interest costs can skew this comparison. These are the reasons that one calculation needs to be made excluding the mortgage and interest numbers.

On the other hand, investment properties are all about the bottom line profit. Your mortgage and interest costs are expenses that come out of gross income. Including these in the calculation is the only way of accurately estimating the profit that the properties will produce.

The cap rate is only the beginning of a thorough due diligence on an income property and should never be solely relied on when making a purchase decision. Financial calculations you want to perform include cash-on-cash return, debt coverage ratio, and return on investment, among others.

Please leave a comment if this article was helpful or if you have a question.

Author bio: Brian Kline has been investing in real estate for more than 30 years and writing about real estate investing for seven years. He also draws upon 25 plus years of business experience including 12 years as a manager at Boeing Aircraft Company. Brian currently lives at Lake Cushman, Washington. A vacation destination, a few short miles from a national forest in the Olympic Mountains with the Pacific Ocean a couple of miles in the opposite direction.

Author bio: Brian Kline has been investing in real estate for more than 30 years and writing about real estate investing for seven years. He also draws upon 25 plus years of business experience including 12 years as a manager at Boeing Aircraft Company. Brian currently lives at Lake Cushman, Washington. A vacation destination, a few short miles from a national forest in the Olympic Mountains with the Pacific Ocean a couple of miles in the opposite direction.