Real Estate Marketing & Beyond

Several mortgage groups are calling on the Consumer Financial Protection Bureau to remove its newly released consumer mortgage education tool, the “Rate Checker,” which was created to help borrowers shop for a mortgage by comparing mortgage rates that lenders are offering.

The National Association of Mortgage Bankers and the Mortgage Bankers Association are urging CFPB to remove the tool, which was rolled out earlier this week. The groups argue that CFPB’s Rate Checker mentions mortgage rates and costs but fails to include disclosure items like the annual percentage rate, closing fees, etc., that are required under TILA-RESPA rules.

“This tool will do nothing but confuse consumers in their shopping experience,” says John Councilman, president of NAMB. “These rates do not account for closing costs, APR, Loan Level Price Adjustments or other key factors. More important than rate is quality of service and closing reputations of others involved in the transaction. If a private company released this exact product, the CFPB and state regulatory authorities would have a team sent in to shut the site down.”

David Stevens, president and CEO of the Mortgage Bankers Association, also has called on the CFPB to remove Rate Checker. “It sets borrowers up for severe disappointment,” Stevens told HousingWire.

In response, the CFPB told HousingWire that Rate Checker is an educational tool and is one of many tools the agency debuted this week to help consumers become smarter mortgage shoppers.

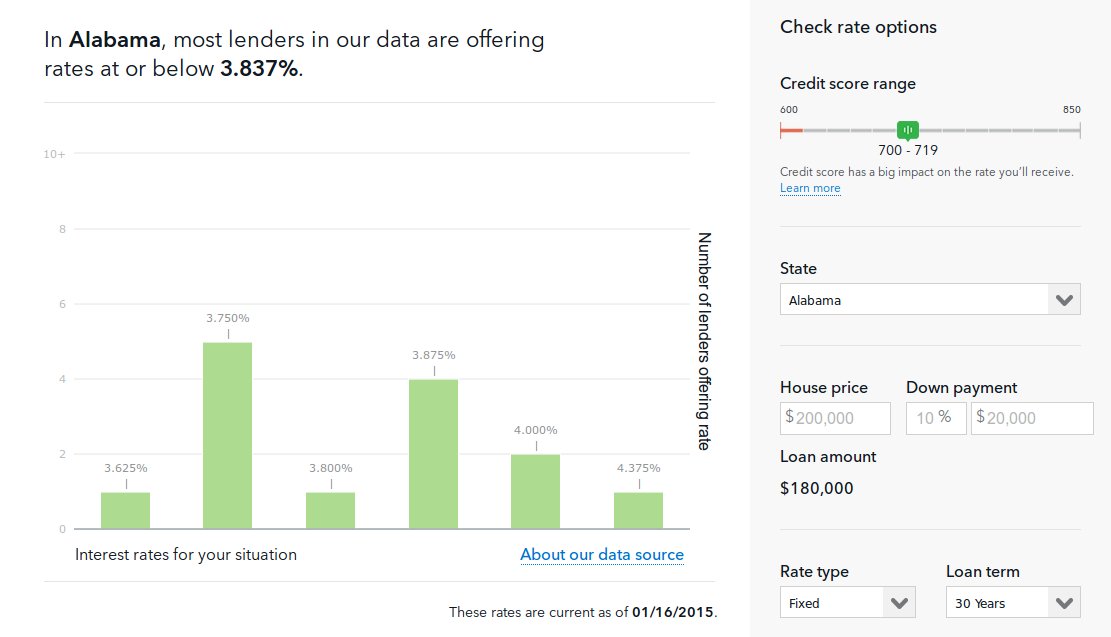

The CFPB has announced no plans to remove Rate Checker from its new online suite of tools called “Owning a Home.” The new interactive page is aimed at helping consumers better understand the mortgage process, compare lenders, and shop for the best deal. A recent CFPB study found that three out of four borrowers fail to comparison shop when looking for a mortgage.

CFPB said in announcing the Rate Checker tool that it will help consumers understand the interest rates available to them based on the same underwriting variables that lenders use, including loan type, property value, loan amount, and credit score. The tool also allows borrowers to compare different interest rates and how much they will cost over the life of a loan, as well as apply different down payment scenarios to see how they would impact the cost of the mortgage.