Real Estate Marketing & Beyond

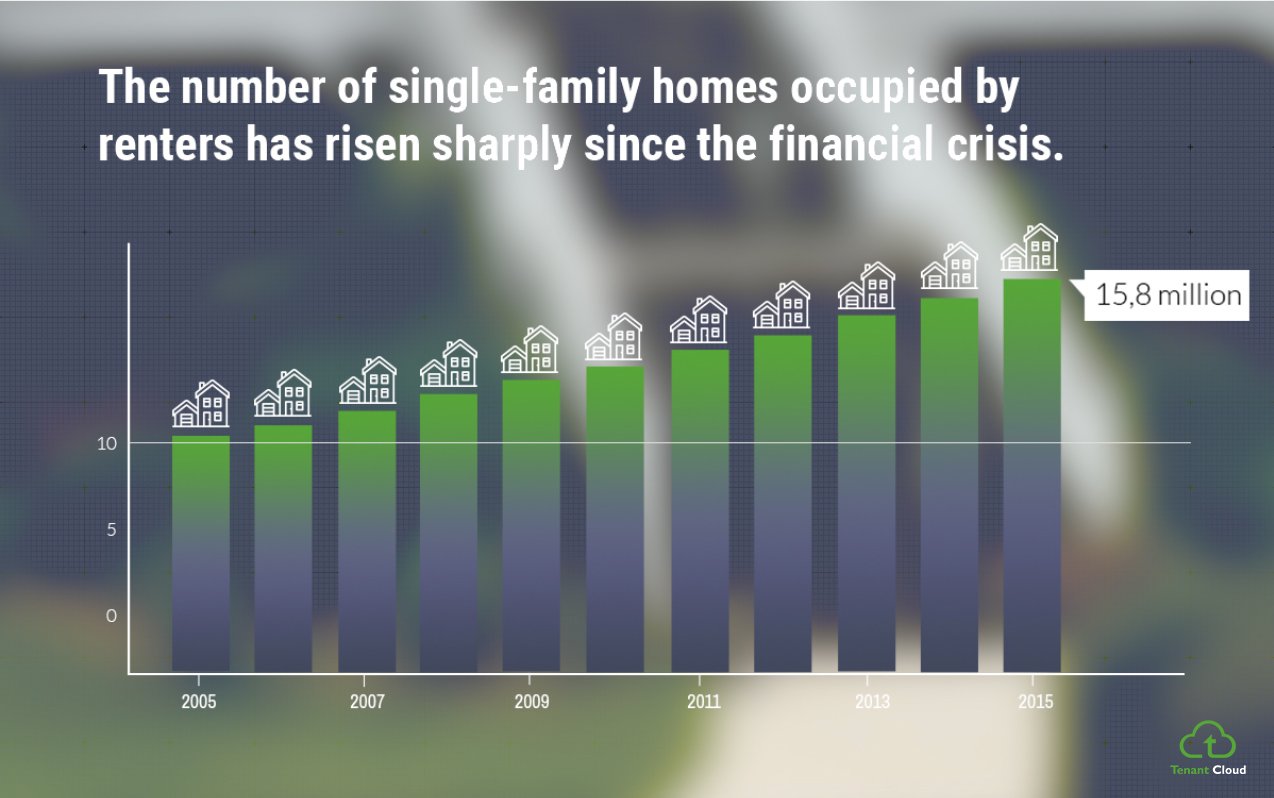

Airbnb is now in over 34,000 cities across 191 countries globally, and the popularity of sites like Homeaway and VRBO is growing steadily. In fact, a recent report predicts the global vacation rental market to be worth $170 billion by 2019. TenantCloud data follows the national trend showing the number of single-family homes occupied by renters has increased sharply. In the past 5 years, it is estimated to have reached nearly 16M in the U.S. alone.

As owners of rental properties know, a major benefit of renting a home are the tax advantages; however, many landlords don’t understand the best way to maximize their tax incentives and as a result, may be missing out on opportunities to make their rental revenue go further.

As we approach this year’s Tax Day, below are the top five tips that landlords should keep in mind when they file:

1. Save it all: Keep track of ALL of your receipts and expenses – which can be easier if you use a software solution that allows you to keep it all online. When making a purchase snap a photo, on your accounting app and add it to the expense. By utilizing cloud-based apps you can make life easier and information more accessible when you want it.

2. Depreciation is your friend: Depreciation is not an annual cash flow expense, but a deduction from your gross rent income. This helps to increase cash flow, while lowering the tax burden. To calculate your depreciation - take the down payment on the house plus the loan outstanding (minus small costs for closing) minus the value of the land and divide by 27.5 to get the amount you can expense each year.

3. Borrowing interest: If you have a loan on your rental, it can have substantial benefits. Borrowing on your rental allows you to combine the depreciation expense with the interest paid on the loan to maximize your cash flow, while also lowering your tax burden. It does it by allowing you to use money that would have been spent buying the house. It also allows renters to make rental payments of which are used to pay the mortgage of the rental house while it appreciates in value.

4. Expense your ride: Your car can be a great value in your rental business. If you drive your car to get supplies for your rental, show your property, review a maintenance request or anytime you’re driving somewhere for your rental, deduct those miles from your rental income. The current allowable deduction is $0.575 per mile, which allows for gas, wear and tear, car washes, etc.

5. Make the most of your office: Remember to expense your regular “office charges,” including your phone bill/plan, Internet, laptop, etc. Other materials and supplies that are used for the rental can be expensed as well. And if you attend educational seminars as part of your rental business, you can expense food and entertainment (50%) for any charges related to your work and time as a landlord.

Owning a rental property is a business in itself, so maximizing the tax benefits available to landlords it the best way to ensure you are making the most of your business and setting yourself and your property up for success.

Joe Edgar is CEO of TenantCloud, the premier cloud-based property management solution that helps landlords maximize the revenue from their rental properties