Real Estate Marketing & Beyond

Every investor should know about the IRS tax code 1031 exchange (1031 is the tax code section if you want to look it up). This part of the tax code allows you to sell one investment property to purchase a higher cost (more profitable) investment without paying capital gains taxes and depreciation recapture taxes. The 1031 exchange can be used in many ways such as selling a property and taking part of the profit out but when most of the profit is rolled over into a new investment you can defer taxes on the amount that is rolled over.

This can be a great way of building a financial legacy for your family. You'll definitely want to seek out the advice of a highly qualified 1031 tax expert but there are ways of combining a 1031 exchange with a trust so that you pass on investment properties to your heirs practically tax free. Your heirs can continue building your investment business without seeing it crippled by high taxes. This is a secret to how the ultra rich keep their wealth.

© aihumnoi - Fotolia.com

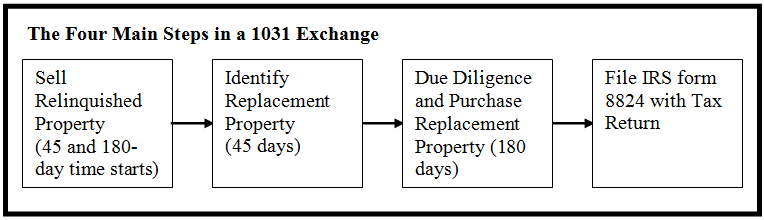

There's no doubt that the 1031 exchange rules are complicated and there are a half dozen or more ways you can improve your investment holdings without paying capital gains or depreciation taxes on sold properties. Here is the basic process.

Those are the requirements for a fully tax deferred exchange. However, you can pocket a portion of the profit and only pay the taxes on the portion of the profit you take out while still deferring taxes on the portion you roll over into the new investment. Below is the simplified version of the four-part process.

Most investors consider the time restrictions the toughest part of a 1031 exchange (especially when commercial real estate is involved). As you see in the process above, there are two strictly enforced time requirements. You must identify a replacement property within 45 day of completing the sale of the property you are exchanging for a better property.

You can identify up to three different properties as possible replacement properties. However, as soon as the replacement properties are identified, the 180 day clock starts ticking to perform your due diligence and close the deal. Missing either one of these time requirements will completely disqualify your 1031 exchange and holidays along with weekend days count.

The other major requirement is that a Qualified Intermediary must be used. This is a person holding a specific license allowing them to make the financial transactions on your behalf. The logic behind this is that you are never allowed to have actual or constructive receipt of the funds from the sale. One other point worth noting is that neither the purchaser of your old property nor the seller of the new investment property needs to directly participate in the 1031 exchange. This all might sound complicated but it's really not once you have an expert guiding you through the process. In the end, your tax savings are enormous because you avoid them in full.

Please leave a comment if this article was helpful or if you have a question.

Author bio: Brian Kline has been investing in real estate for more than 30 years and writing about real estate investing for seven years. He also draws upon 25 plus years of business experience including 12 years as a manager at Boeing Aircraft Company. Brian currently lives at Lake Cushman, Washington. A vacation destination, a few short miles from a national forest in the Olympic Mountains with the Pacific Ocean a couple of miles in the opposite direction.

Author bio: Brian Kline has been investing in real estate for more than 30 years and writing about real estate investing for seven years. He also draws upon 25 plus years of business experience including 12 years as a manager at Boeing Aircraft Company. Brian currently lives at Lake Cushman, Washington. A vacation destination, a few short miles from a national forest in the Olympic Mountains with the Pacific Ocean a couple of miles in the opposite direction.

Nice article on an important topic for creating and maintaining wealth in real estate.

For low cost Qualified Intermediary services-$399 Exchange.

Mimi,

Thanks for pointing out this is a way to preserve wealth as well as a way to build it.

Brian Kline

Very nicely written article Brian. We are constantly amazed how few owners of investment real estate even are aware of Section 1031 of the US Tax Code. Most of what we do as Qualified Intermediaries is education and strategy. One thing you mentioned in your article is that there are licenses required for professionals that handle exchanges. There is only one state that currently requires licensing, and that is Nevada. There are a few other states that have adopted regulations and guidelines surrounding exchanges. It is extremely important that investors do their due diligence on their Qualified Intermediary as vigorously as they select the other professionals they work with. Our trade organization the Federation of Exchange Accommodators (FEA) is very useful in assisting investors in locating good firms. They also are very active in working with the states in enacting solid rules policies to protect the consumer.

John,

Thanks for the additional information. I was under the impression the IRS had a requirement that Qualified Intermediaries have a license.

Brian Kline

National 1031 exchange - qualified intermediary.

The article states, "However, as soon as the replacement properties are identified, the 180 day clock starts ticking to perform your due diligence and close the deal." This is incorrect!!! The time period for the '180 day clock' starts on the day the relinquished property closes, the same start date as the 45 days to identify replacement property.

Mark,

You are absolutely correct. I noticed my error after publishing the article. Thanks for pointing this out.

Brian Kline

Great article. Very helpful.

Thanks Dorothy. Always good to learn that information is useful.

Brian Kline