Real Estate Marketing & Beyond

It takes around 11 months for a consumer’s credit score to recover after purchasing a home, a new study by online loan marketplace LendingTree has found.

When a consumer buys a home, their credit score drops by an average of 15 points, but only after 160 days, or just over five months. That’s because it takes some time for credit reporting agencies to add the transaction to consumer’s records and adjust them for that purchase.

LendingTree’s analysis also revealed it takes another five months following that drop for credit scores to recover. In total, it takes the average borrower around 161 days before their credit score reaches its former level. All in all, it takes around 11 months for their score to get back to where it was after buying a home.

“When a consumer takes out a mortgage, a large balance is added to his credit report,” researchers from LendingTree explained in the report. “Credit scoring models consider a consumer’s total balance of money owed, and a large increase in outstanding debt drives scores lower. The presence of a new credit line item also weighs on the score, though to a lower extent.”

However the credit score recovers fairly quickly once the borrower starts making one-time payments on their mortgage. In addition, having a mortgage also boosts the diversity of accounts in a consumers’ credit file, eventually leading to an increase in their score.

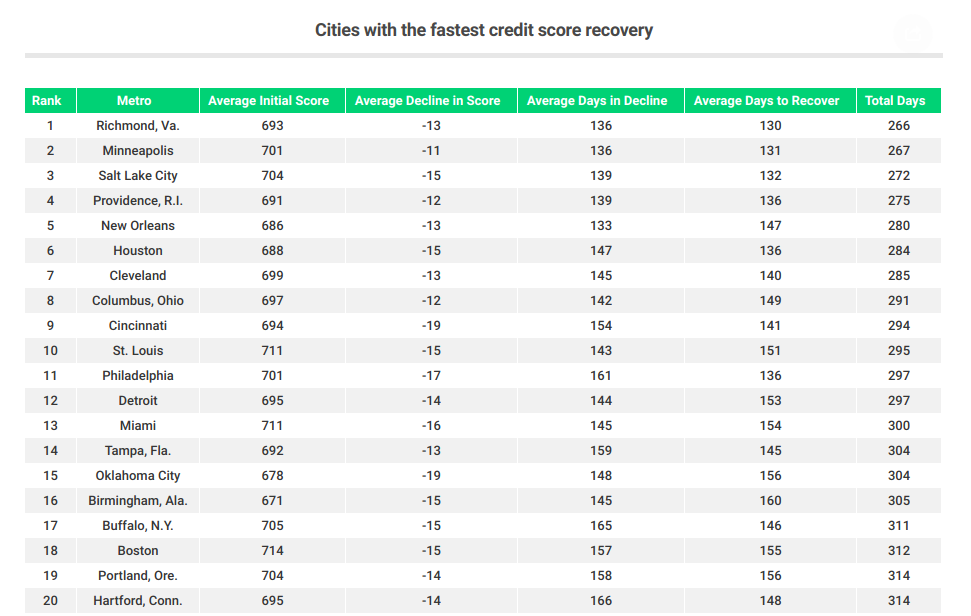

LendingTree researchers evaluated the variation in credit scores across the country’s 50 largest cities to find where home buyers saw the fastest recovery to their credit scores after getting a mortgage.